Gross Margin is perhaps of the most followed metrics when evaluating software companies. Investors and companies themselves are absolutely obsessed with it

In this article, we break down Gross Margin to figure out what drives it, and whether companies are actually rewarded for having a good gross margin.

In my last article, I explored the relationship of Sales and Marketing expenditure to examine whether there is an ideal ratio of spend. Today, we’ll use this knowledge and apply it to Gross Margin.

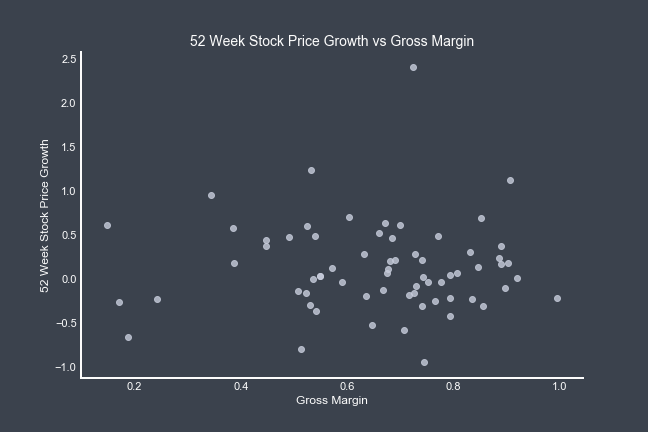

Does Above Gross Margin lead to Stock Success?

To answer this simply, if we simply plot Stock Returns against Gross Margin and run a simple linear regression, we can see that there’s no relationship between Gross Margin and stock returns. Absolutely none - R^2 of 0.

How does one increase Gross Margin?

In the last article, we explored the relationship between Sales and Marketing expenditure vs revenue. Clearly, there are two ways to increase Gross Margin:

- Increase Revenue

- Decrease the Cost of Revenue

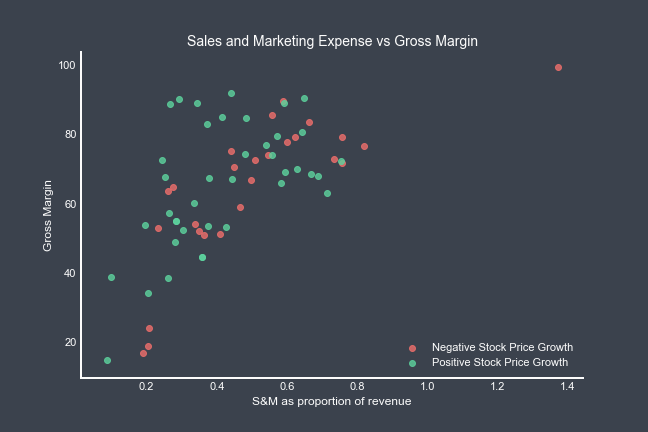

I modelled in my last article that both R&D and S&M spend contributes positively to increasing top-line revenue, so I was intrigued to see the spread of S&M and Gross margin.

Again, making a simple plot we can see that there is a positive relationship between S&M spend and Gross margin, albeit diminishing returns style. This intuitively makes sense.

Standing out from this graph, I like the look of the cluster of companies who achieve higher than 80% Gross margin but spend less than 50% of their revenue on Sales and Marketing - they appear efficient. Since this cluster includes companies such as Disney (DSNY), Intuit (INTU), Citrix (CTXS), Paycom (PAYC) and others, helps to rule out the possibility that I’ve found a sub-industry.

All the companies in this cluster performed well, and, on average, performed better than the other companies in this cohort. Every company experienced double digit stock price growth, with an average stock price growth of 28% compared to 10% for the other companies.

Revenue growth difference was smaller, likely due to the restrained spend of Sales and Marketing expenditure.

The role Gross Margin plays

By definition Gross margin is an efficiency metric. From this analysis, we can view it more as a health check metric. In my mind Gross margin should never be a target, but instead is a scorecard of operational discipline.

In this, we uncovered that a Gross margin figure alone isn’t enough to warrant stock price growth. While Gross margin can be inflated by increasing Sales and Marketing spend, we see successful companies keeping control of the Sales and Marketing spend - subsequently keeping Cost of Acquisition in check.