There is a lot happening in New Zealand’s economy currently. New Zealand is officially in a recession with new GDP figures that came out yesterday, a monetary policy update is due next week and an election is taking place mid next month.

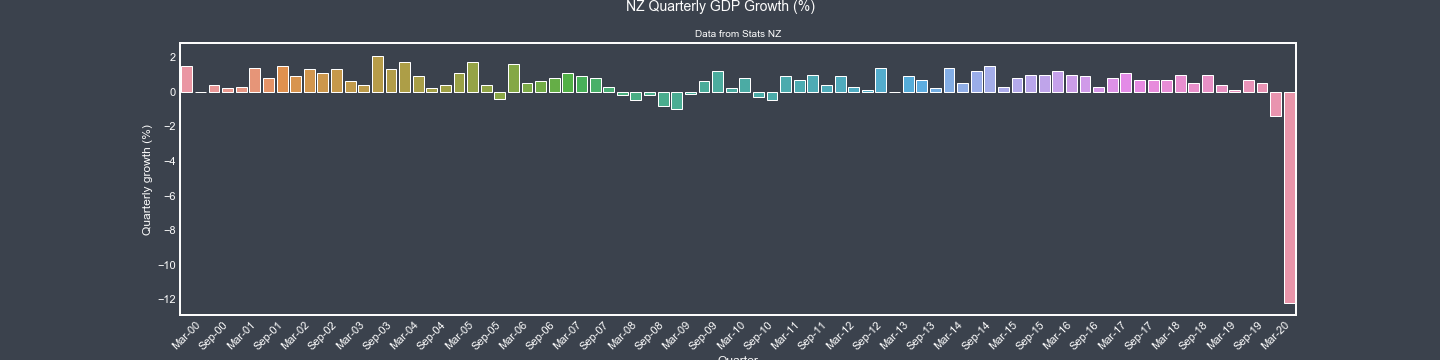

Thursday’s numbers from Statistics New Zealand represented a -12.2% reduction in GDP for the June 2020 quarter - the largest quarterly fall in GDP on record. Which, unlike the previous quarter’s figures only captured a week or two of New Zealand’s nationwide 4-week lock down, June 2020 figures captures the lion’s share of the lock down.

Monetary Policy: The Stress Test

With little wiggle room in monetary policy, the Reserve Bank of New Zealand (RBNZ) released a Stress testing report aimed to provide confidence to businesses and consumers.

In the report, they model the banks resilience under two scenarios:

- A one-in-50 to one-on-75 year sitauation

- A one-in-200 year event.

Both sitatuions are significantly worse than the current economic situation.

In the one-in-50 to one-in 75 year event, it sees a rise in unemployment to 13.9% (currently 4.0% for the June 2020 quarter) and a fall of 37% in housing prices.

Under this scenario RBNZ conclude that all banks remain above the regulatory minimums, and will remain resilient given these conditions.

Bank stability, or more broadly confidence in banks is a crucial factor in recessions. A loss of confidence can cause bank runs as people rush to withdraw their funds - depicted in the header image above of a bank run in the 2008 crisis. This report is an interesting one, and is the RBNZ flexing their position to go beyond sole monetary policy.

Of course, this report simply speaks to the effect on banks. A 37% reduction in house prices will cause severe economic damage, and we can expect a large increase in home loan defaults causing not isolated to banking.

The loan-to-value ratios over the ‘good years’ have meant home-owners generally have a more equity in a house when compared to the 2008 crash, which should help reduce home loan defaults. (This has been explored more in a recent post about Loan-to-value ratios here)

On the more traditional monetary policy side, there’s no real appetite to even consider increasing interest rates. Low interests facilitate, but can’t force increased economic activity.

With interest rates already at an all time low (Official Cash Rate currently 0.25%), nearly all analysts, and myself predict that the RBNZ will look to hold the Official Cash Rate in the coming week. Reports such as the above, are a testament to the RBNZ flexing powers outside of the Official Cash Rate.

Confidence in the Economy

ANZ’s Consumer confidence index took a slight dip in August 2020, easing 4 points which is well under the historical average. This comes as it was discovered COVID-19 is back in the community.

Overall consumer confidence has recovered nicely from the COVID lows seen during lockdown. 27% of consumers expect to to be better off financially this time next year, and only 3% of consumers think it’s a bad time to buy a major household item. Given the lockdown and economic conditions - these are pretty positive indicators.

Net Migration is a potential positive

New Zealand has been viewed as a leader with its COVID-19 response, boosting its popularity and sparking criticism from Donald Trump. As a result of uncertainty in the world, and the relative certainty in New Zealand, New Zealand has experienced record highs in Net Migration from returning Kiwis. Although, this appears to have slowed down in month of July.

Net migration creates demand for housing in New Zealand. Increased migration, bolstered with low interest rates are expected to minimise the risk of significant house price drop.

Income and Employment

Other forces pushing down house prices, are largely employment related, both unemployment and income levels. Effects of unemployment and lower income levels causes ripples beyond housing prices, including:

- Lower consumption spending

- Lower tax revenue collected from Income and GST.

The primary response to reducing unemployment growth has been through wage subsides. Current wage subsidies support 575,000 businesses and 1.7m worker - just over 60% of the workforce.

Treasury states that the wage subsides have been more effective than they had originally foretasted. Despite this, Treasury in their Economic Outlook expect a rise in unemployment - albeit not as severe as their Budget Update 2020 report.

No-one knows what will happen to business once the subsidies end, it is natural to assume we’ll see a spike in business shut-down. However, there is a consensus that the longer the government can sustain wage subsidies, the more time businesses have to recover giving them a better chance of survival post subsidy.

It’s early days in this economic downturn, with additional complexities such as tight borders causing a lack of international tourism, it will be a different downturn to what we’ve seen previously.

Unfortunately, it seems that our most valuable industries, tourism, retail and hospitality will always be the first, and hardest hit should COVID-19 return.

It’s hard not to focus on quarter by quarter thinking, but the economy needs a clear long-term recovery plan to keep confidence high.